- Fintech opportunities in Japan include cashless payments, blockchain solutions, and regional banking digitisation

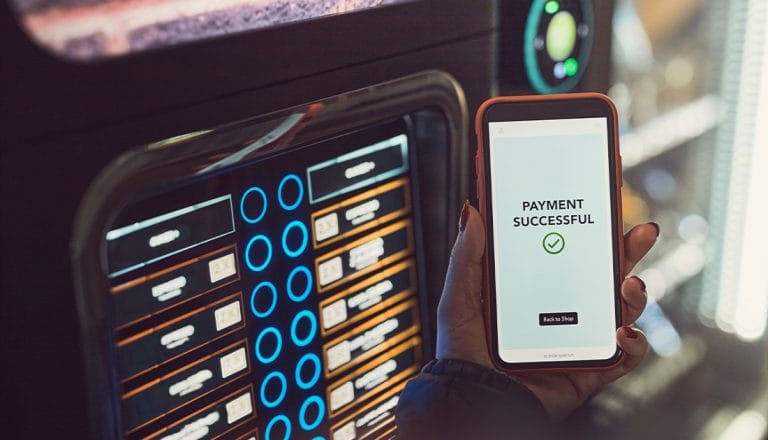

- Nearly 43 percent of payments made in Japan are now done through cashless methods

- The government views fintech as a catalyst for larger digitisation efforts and has created policies supporting the sector

Japan has long been a country that prefers physical to digital. This mindset extended to banking and financial services, where cash has remained popular despite widespread digitisation elsewhere in Asia. However, the pandemic brought about a surge in interest in fintech, and the Japanese government now wants to build on existing momentum. Asian Insiders Japan Partner Haruna Shino shares insights on these developments as well as the fintech opportunities currently available in Japan.

When former Finance Minister Taro Aso announced that the Ministry of Finance would focus more on nurturing the fintech sector as opposed to regulating it in 2016, there was hope the industry would take off. The proclamation was made around the time Japan eliminated restrictions on how much money domestic banks could invest in Fintech companies.

Some progress has been made, but Japan continues to trail many other Asian countries when it comes to fintech. One of the largest obstacles has been moving away from being a cash-first society, although the government recently reached an important milestone in that regard.

More than 40 percent of payments made in Japan are now cashless, and the goal is to have this figure reach 80 percent. If it were to be achieved, the country would be the global leader in cashless payments.

Even with the success of current efforts, reaching the 80 percent target will require more work. A reminder of this can be found in the form of ATMs which are still prevalent across the country, including inside Japan’s robust network of convenience stores. According to a 2023 report from We Are Social and Meltwater, the country is behind the global average in terms of digital payment usage. Given consumer preferences, there had been little incentive for banks to embrace fintech.

To that end, the sector has an estimated market value of USD 10-12 billion. This is an increase from the start of the decade but still relatively small when compared to countries with similarly sized economies. There are, however, signs further growth can be expected.

Changing perceptions

Resistance to fintech has weakened in recent years as the government, banks, and the public began to realise the benefits it can bring. Starting with the former, policymakers view the sector as a core component of its digital transformation ambitions. In 2018, the Ministry of Economy, Trade, and Industry announced a 2025 target to have 40 percent of payments happen through cashless methods. This goal appears to be in sight after surpassing 39 percent in 2023.

For banks and financial institutions, they now better understand the cost savings and service improvements fintech can provide. Mitsubishi UFJ Financial and Mitsui Sumitomo Financial Group have plans to close physical branches while investing in digital initiatives. Some regional banks are following suit with widespread digitisation that will allow them to better serve consumers.

Finally, Japan’s younger population is becoming increasingly comfortable using mobile phones to make payments and conduct various banking activities. The pandemic spurred much of this sentiment as fintech services increased by 85 percent over the past few years, one of the highest totals globally.

Policy supports fintech

Fintech opportunities in Japan are supported through favourable policies now in place. The process began in 2018 with a revised Banking Act taking effect. The updated policy included a mandate for all banks in the country to develop application programming interfaces. Additionally, it created a more transparent framework on how services provided by fintech firms could utilise financial institution data.

Elsewhere, the Financial Services Agency launched sweeping fintech policies designed to protect consumers, improve transparency, promote competition, and ensure sector supervision.

Improvements have also been made to the Zengin System, the network that connects banks digitally and clears funds following the transactions, in an attempt to provide greater access to fintech businesses.

In October 2024, British company Wise became the first foreign fintech entity given direct access to the Zengin System.

Finding fintech opportunities in Japan

It must first be noted that many fintech opportunities in Japan are connected to banks in one way or another. While attempts have been made to reduce their influence on the sector, the bulk of demand for solutions and new technologies comes from there. On a positive note, many are aware of the need for innovation and are open to potentially working with overseas entities who can assist in key areas.

Cashless payments – The country has made some progress on this front but remains well behind the pace. If the government is to reach its target of an 80 percent cashless payment rate, more work must be completed. QR code payment systems could be the most exciting development. The digital payment method continues to see growth in terms of Japanese users, but competition in the space remains open.

Regional banks and credit unions – These account for more than 60 percent of core banking services in Japan but have been unable to keep up with the country’s digitisation push. The Bank of Japan noted in a 2021 whitepaper that regional banks would be best served by partnering with fintech companies capable of improving operations, reducing costs in critical areas, and increasing profitability. Foreign fintech companies boasting proven technologies are recording success in this segment.

Blockchain – This is Japan’s most advanced fintech segment, but opportunities here are still available. Smart contracts connected to automated payment processing, such as the case of probate, remain underdeveloped.

Silver solutions – Japan is an aging society, and that brings with it unique challenges, some of which can be addressed by fintech. Solutions capable of addressing healthcare financing and payments, wealth transfer, and pension-related services are in demand.

Final thoughts

It is commonly believed that entering Japan is difficult for businesses, especially those in fintech given the country’s struggle to digitise over the years. In reality, understanding the local market and having a well-researched entry strategy can ensure you overcome those obstacles.

Foreign fintech companies can succeed in Japan if they can demonstrate how their products or services are beneficial. Banks and financial institutions are notoriously risk-averse and value a proven track record.

Finally, having a local partner who can navigate some of the complexities, including the language barrier and regulations, that come with entering Japan is highly recommended.

For a no-obligation call to discuss fintech opportunities in Japan, please contact Managing Partner Jari Hietala: jari.hietala(at)asianinsiders.com or Haruna Shino, Japan Partner:

haruna.shino(at)asianinsiders.com